Will the Housing Market Crash Again Next Recession

Domicile prices are skyrocketing, housing inventory is at best lows and homebuyers have to fence with multiple bids. Tin can this last? No, it tin can't. In fourth dimension, markets always find balance and balance is a proficient matter. But, that doesn't mean housing is going to crash.

One of the reasons that I moved into the "team higher mortgage rate" camp is that what I saw in January, February, and March of this year was so unhealthy that I labeled the housing market place savagely unhealthy.

I set up a specific domicile-cost growth model for the years 2020-2024 that said if home prices simply grew at 23% during this v-year period, the housing market place would still be OK, given wage growth. Obviously, my home-price growth model got smashed! With where prices were heading when mortgage rates were under 4%, nosotros were looking at 35%-40% cumulative home-toll growth in but 3 years.

That isn't a good matter, then I desire to see a cool downwardly in prices. However, a cool-downwardly in prices is not the same thing equally a housing crash. Let'due south have a look at what information technology would take to crash homes prices in America.

A few things in life are constant: the sun rises, nosotros will all dice anytime, and every year people say housing is going to crash. Also, people always say we are about to go into recession and that the dollar is going to collapse any mean solar day now! I believe in economic models and I'thou not going to throw up a few charts without forecasting models, considering I want to show the pathway for these things to occur. We have to take everything i day at a time and add new variables when appropriate.

After writing the America is Dorsum recovery model on HousingWire, I wrote an article on my web log about what it would take to crash dwelling house prices on April 10, 2020. Economic vision is disquisitional when forecasting what would happen back then, because those were some of the darkest economic days I can call up. Still, some of usa had faith in our economic models.

COVID-19 happened right at the start of 2020; this is also the menstruum in time when i had forecast a five-twelvemonth once-in-a-lifetime flow for housing to kickoff. The years 2020-2024 were e'er going to be unlike from 2008-2019. As information technology turned out with COVID, we had the most significant housing demographic patch always recorded in history, with the lowest mortgage rates always recorded, and homeowners, on paper, have the best financials ever.

With that said, let'due south look at what needs to happen for home prices to to crash. Hither's a point-by-point comparison of what I said before April ten, 2020 and where we are today.

Inventory velocity

Apr ten, 2020: Nosotros needed a lot of inventory, fast

The velocity of inventory ascent in the next three months is express. It should increment with a longer duration fourth dimension to sell a home. However, unlike in 2006 when need was getting weaker and inventory was higher up six months, it's the contrary now during the B.C. (before COVID) phase. Nonetheless, for A.D. (after the disease), this is why lockdown protocols take to stay on for much longer. This will then mean that demand gets hit for a longer duration.

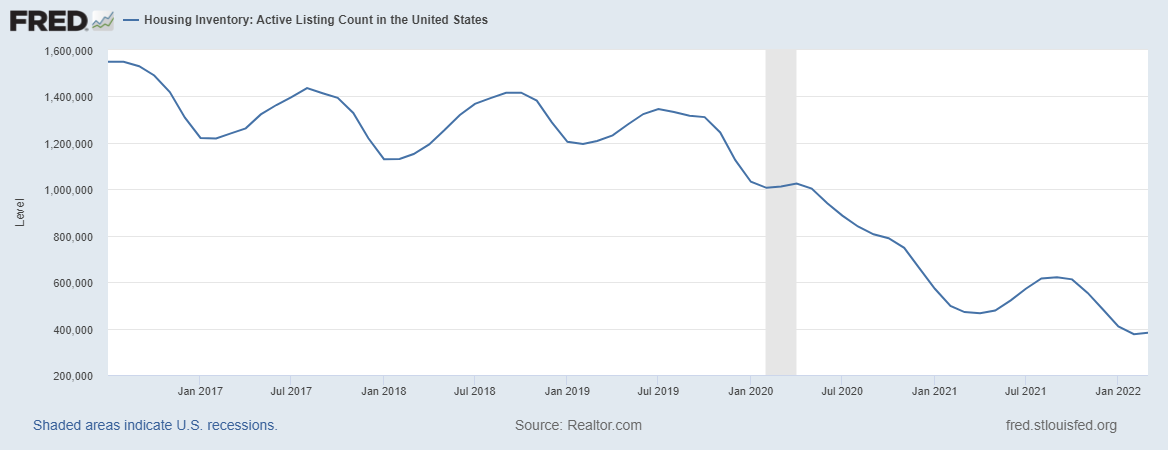

April 2022: Inventory has not recovered.

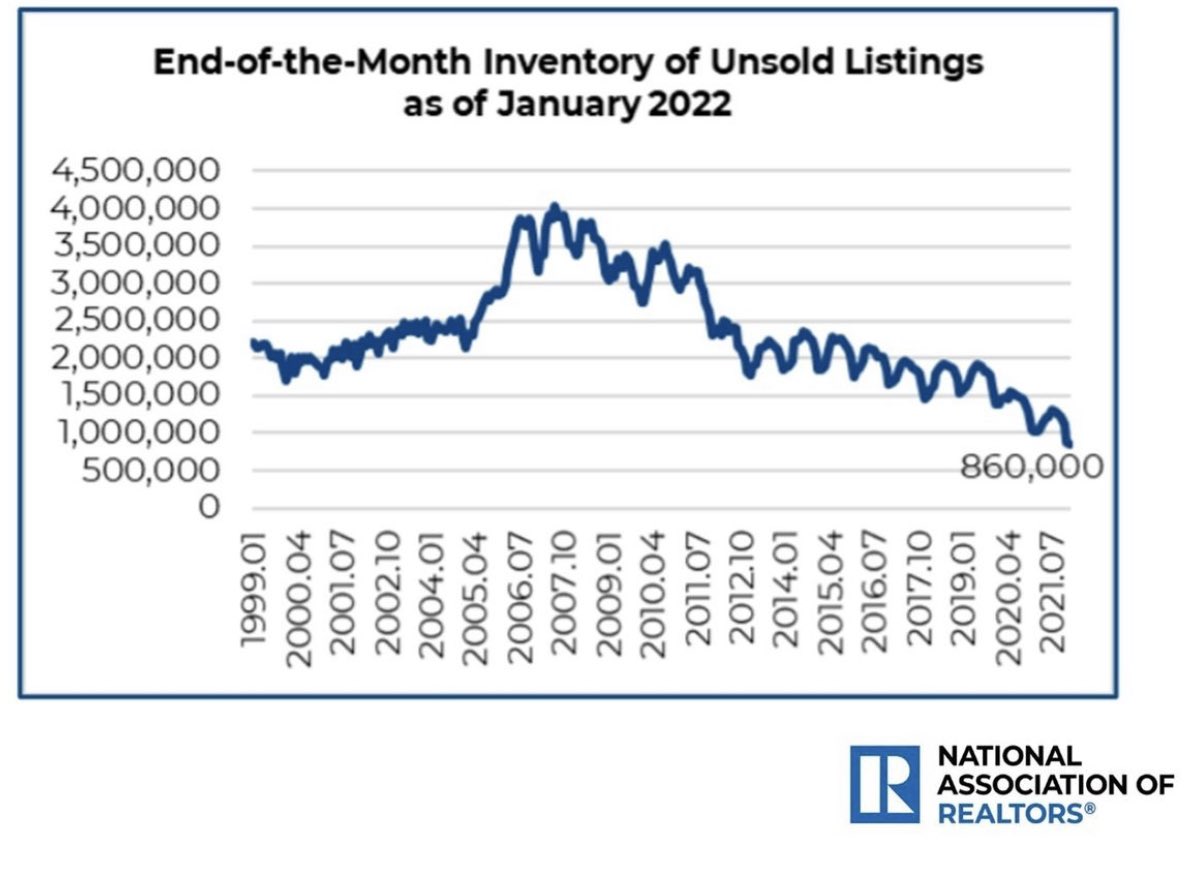

Inventory collapsed in 2020, 2021 and 2022. Nosotros still have negative year-over-year inventory information, which is why I have labeled this is a savagely unhealthy housing market place. My goal is for the full inventory to get back to i.52 -1.93 million — once that happens, I tin take the unhealthy label off the housing market.

We need prices to fall this twelvemonth, next year, and in 2024 to ensure nosotros are under 23% cumulative price growth for 2025. With inventory collapsing, we are in big trouble.

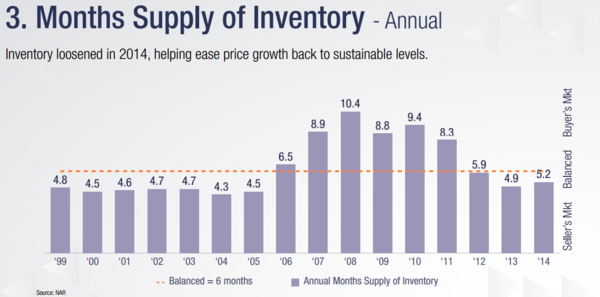

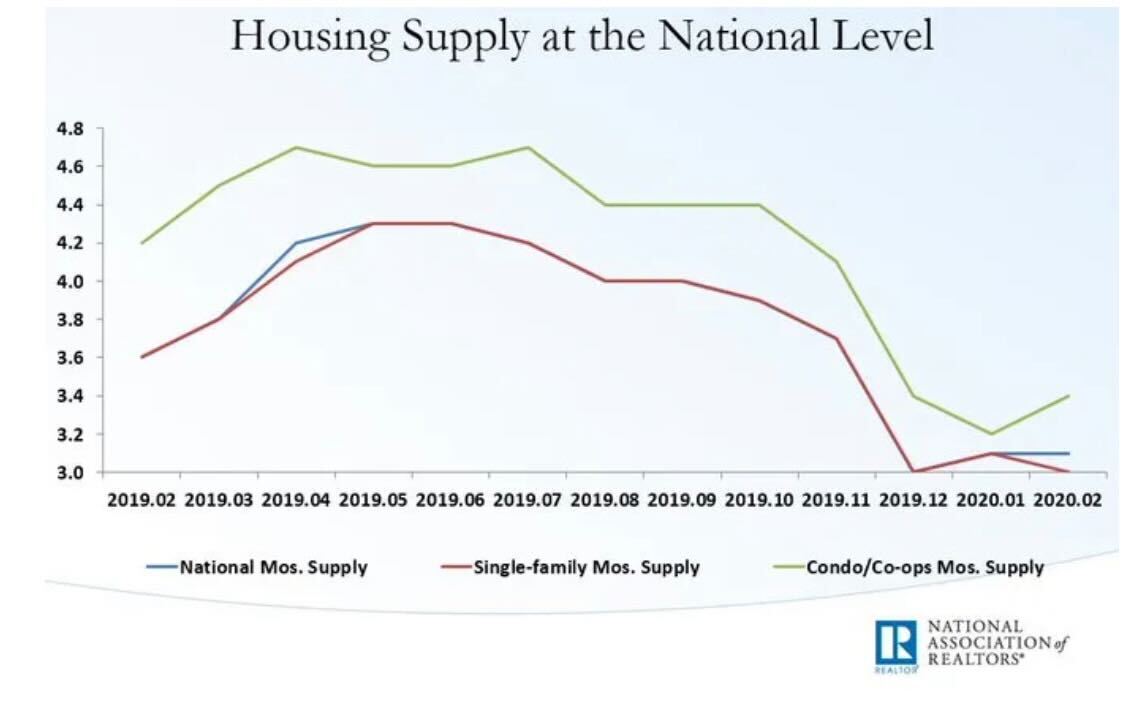

Nosotros are in the part of the year that inventory typically increases. We want the inventory to exist positive year over yr, not negative! If you lot're looking for a housing crash, y'all need inventory to skyrocket with no demand bidding. Monthly supply data being at one.vii months isn't going to practise that. As you lot tin encounter higher up, the monthly supply in 2006, 2007, 2008, 2009, 2010, and 2011 was above six months on average, running at 8.71 months during this six-year period.

April 10, 2020: We had bicycle highs in demand with the inventory at cycle lows.

Inventory levels during this time of lockdown protocols start from a much dissimilar spot than in 2006. Also, the demographics for housing look solid every bit the biggest age group in U.Southward. history are ages 26-32, and the first-time median home buyer historic period is at present 33.

Apr 2022: If anything, demand is higher and inventory is lower.

We are currently at i.vii months, so if you're looking for housing to crash, you will demand to see a lot more total inventory and monthly supply data to skyrocket in a brusk time.

April ten, 2020:

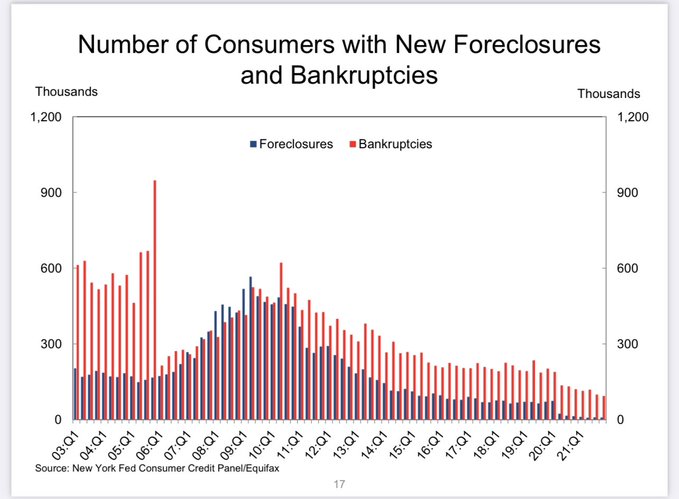

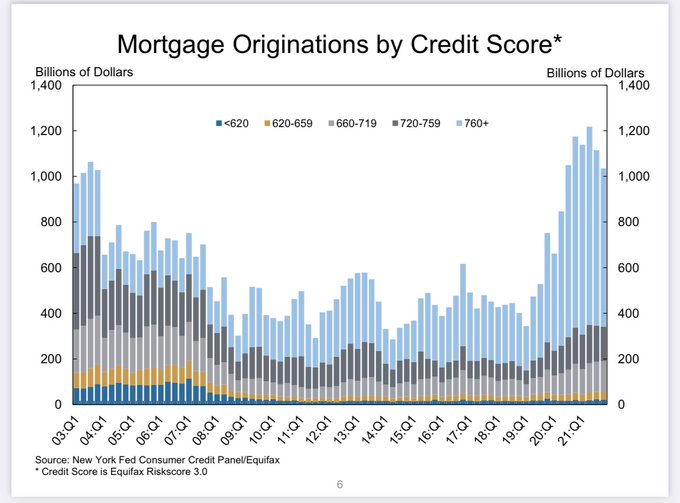

Due to timing, this would have to be a 2021 story. Foreclosures are a long procedure. The government is going to try its best to forbid equally many foreclosures as possible. Even if yous see a noticeable rise in delinquencies, this doesn't hateful distress bulk foreclosure buying is about to happen in one to two months. Due to the forbearance factor in 2020, I would keep an centre on this in 2021 for sure. The legit loftier-level risk homeowners are 2018/2019 and 2020 FHA homebuyers because they lack selling equity, and they would brand up that smaller portion of sub -60 FICO score domicile loans bought in this wheel.

April 2022: At that place was no abstinence crash.

The abstinence crash bros whiffed, non in a pocket-sized way, just in the most prominent fashion ever recorded in history. Not merely did the epic housing crash they called for non happen, dwelling house prices overheated in 2021 so much that the housing market place became really unhealthy.

I warned about this on Bloomberg Financial in January of 2021. Over the years, a considerable portion of my economic piece of work has revolved around housing credit. Having a dull housing debt market place was the best thing for the U.S. housing market, and we should never ease lending standards to try to facilitate demand. Lending standards are already liberal enough, so we don't need to go downwards that avenue.

Belatedly cycle lending is always a hazard in the lending industry. People who buy a home belatedly in an expansion, with a low down payment buy, into a falling market place risk a short sale or foreclosure. Outside of that risk, everything else is fine.

Again, what happened in housing from 2002 to 2008? We had a credit smash. Credit worsened from 2005 to 2008. So, subsequently all that, the job loss recession started. Our market is much dissimilar than that 2002-2008 period.

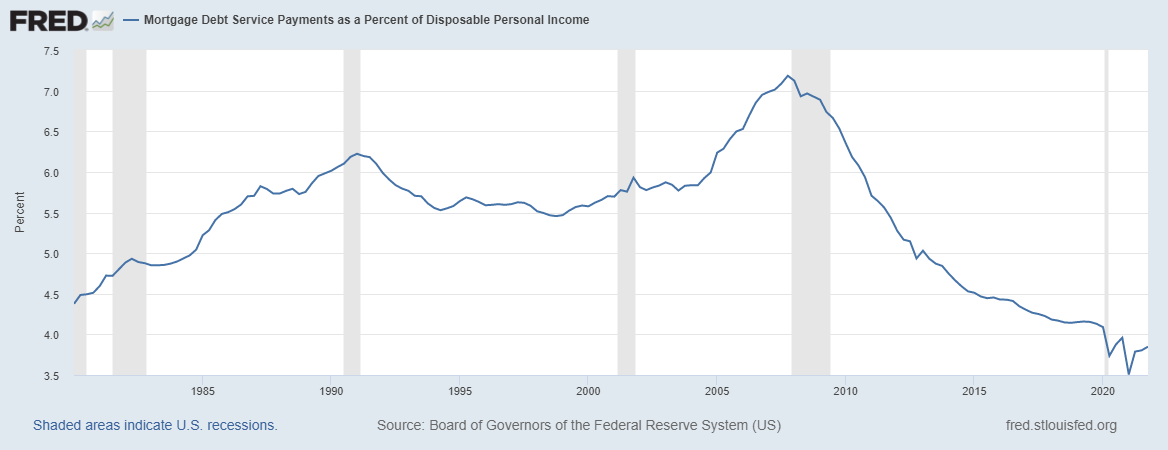

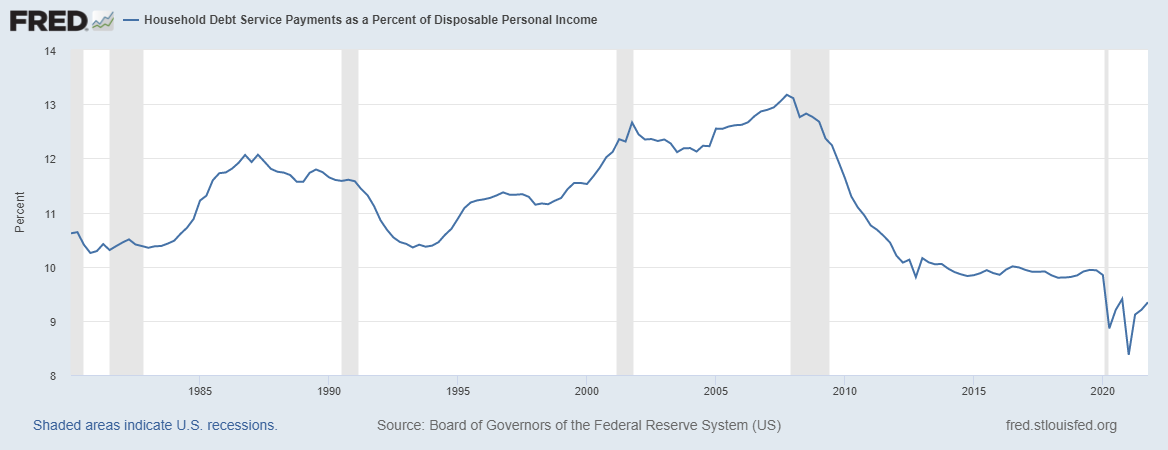

The cash menses of Americans is ameliorate than ever right now: They have had a fixed depression debt cost over the years, refinanced multiple times and all as their wages accept been rising.

So, the bulk of the housing stock of owners is in not bad shape. Yous don't take to worry about a mass foreclosure coming from them.

Since mortgage debt is the most significant debt in America, household debt data looks not bad; these two charts were updated this week.

On top of all that credit payment information which looks slap-up, the nested equity position looks fantastic.

From the great Len Kiefer, deputy master economist from Freddie Mac:

If we see credit stress in the data, nosotros will exist able to talk virtually it. Notwithstanding, if it doesn't happen until the next recession, late-cycle lending is really your only hazard. And who knows, maybe the government volition run an abridged version of forbearance from at present on to make certain families' lives aren't destroyed.

Time will tell on that. However, late-bike lending is e'er a gamble for brusk sales and foreclosures. This would exist forced selling, unlike the unhealthy forced bidding we have now in the current housing market. Again, first-world problems for sure.

Equally someone who wants to see home prices fall, I am keeping an heart on all this. However, if you're waiting for dwelling house prices to go dorsum to 2012 levels like the Housing Chimera Boys 2.0 have been saying since 2012, the post-obit is what you would need:

1. Inventory increases on a massive scale, over six months of housing supply with elapsing, and full inventory levels skyrocketing equally nosotros saw from 2006-2011.

As of right now, I am praying every day that inventory just gets back to 2019 levels

two. Need to drib and driblet fast, with no market bid for homes, assuasive inventory to rise at a faster pace.

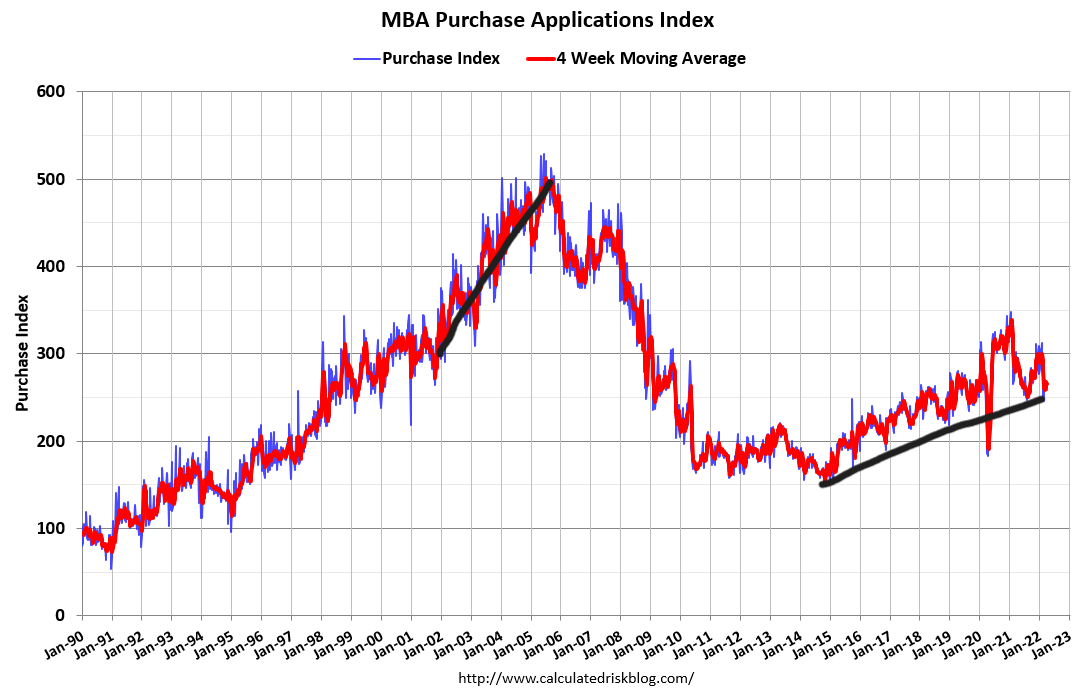

I oasis't seen too much difference in the year-to-date tendency in purchase applications trends. Later on making some COVID-19 adjustments to this yr'south data, which I believe concluded in mid-February, I tin can come up with only a 2%-4% impact year over yr so far from the offset of the year.

For case, two weeks ago, purchase awarding information was up 1%, and this week it was down iii% week to week. The yr-over-yr data is down 9% this week, simply recall, this data line has been negative since June of 2021 on a year-over-yr basis.

Due to the rapid home-price growth in 2020-2022, I believe college rates should absurd downwardly the housing market. Don't forget the mortgage buyer is the about significant homebuyer out there; they affair the about. I believe some people who say that iBuyers and Wall Street investors are holding upward the housing market don't understand they're making a super bullish thesis that housing can't ever fade.

Higher rates have ever created more days on the market and cooled downwardly toll growth; it should non be any dissimilar now working from some extreme dwelling house-price growth levels.

Withal, if you're looking for home prices to crash, you demand buy application data to exist down twenty%-30% twelvemonth over year for some time, with no recovery like we saw at the end of 2006 toward the bottom end trend between 2010-2012.

For housing to crash, yous would besides need rates to stay high, which ways you don't want the economy to get into recession and have bail yields head lower again. You would have to have housing to crash offset, and so have a job loss recession such as what we saw from 2006-2008. Good luck with that, past the mode.

The sustainability of the housing market place is critical, then home-price growth needs to cool down. Since I lost my v-year cumulative 23% home price growth model in ii years, I hope the market takes a breather.

As I wrote in 2020:

These are night times. But fifty-fifty in nighttime times, nosotros are preternaturally prepared to run across the lite at the end of the tunnel. We learned in the human physiology course that the photoreceptors of the human eye could observe a single photon of lite. While it may not be until nine or more photos hit the retina that we perceived light, we detect before we tin can perceive. Too, if we are diligent, we will exist able to identify the return of hope and light coming dorsum into the American economic system before it is perceived by all those poor masked souls effectually us.

jessopscrepativen1988.blogspot.com

Source: https://www.housingwire.com/articles/what-would-it-take-to-crash-the-housing-market/

0 Response to "Will the Housing Market Crash Again Next Recession"

Post a Comment